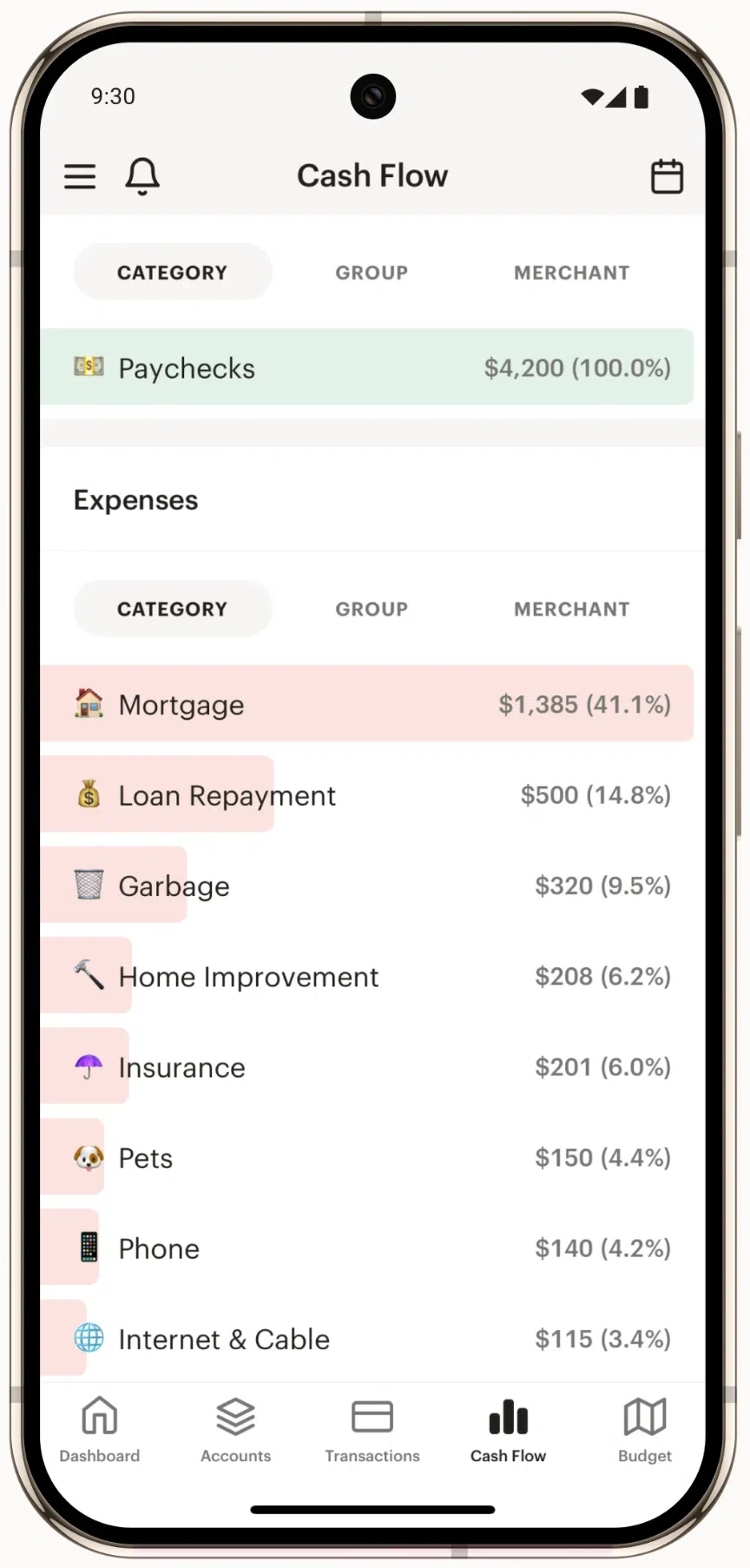

Set up your cash flow first

Childfree households often face a different financial reality than families with children. Without the predictable costs of schooling, childcare, or pediatric care, disposable income tends to run higher, but the risk profile shifts toward lifestyle creep and lack of long-term care planning. Establishing a rigorous cash flow system is the first step in financial planning without children 2026.

Start by tracking every dollar for 30 days. Most childfree couples or individuals underestimate how quickly discretionary spending can slip into fixed commitments. Use a zero-based budget where every dollar has a job before the month begins. This discipline prevents the "surplus" from vanishing into vague savings or impulsive purchases.

Childfree households often have 20-30% more disposable income than families with children. Use this gap to accelerate debt payoff or investment contributions.

Build an emergency fund that covers six to twelve months of expenses. While traditional advice suggests three to six months, childfree individuals often lack the informal safety net of adult children. Your network may include friends or partners who cannot provide financial support in a crisis. A larger cash buffer protects against job loss, medical emergencies, or elder care responsibilities for aging parents.

Automate this process. Set up automatic transfers to a high-yield savings account the day after payday. Treat savings as a non-negotiable expense. Once your cash flow is stable, you can aggressively direct the remaining surplus toward high-interest debt or tax-advantaged investment accounts.

Maximize retirement contributions

Without the recurring costs of raising children, you have a unique advantage: discretionary income. For childfree adults planning for 2026, this flexibility allows you to aggressively fund tax-advantaged accounts that might otherwise be out of reach. The goal is to build a nest egg large enough to support early retirement or sustained luxury travel, rather than just maintaining a comfortable standard of living.

Boost 401(k) and IRA contributions

Start by maximizing your employer-sponsored 401(k). In 2026, the catch-up contribution limit for those aged 60 and older is significantly higher, allowing you to contribute up to $11,250 extra on top of the standard limit. If your employer offers a match, ensure you are contributing enough to get the full match—it is effectively free money that compounds immediately.

Simultaneously, maximize your Traditional or Roth IRA. If you are in a high tax bracket now, a Traditional IRA lowers your current taxable income. If you expect to be in a similar bracket in retirement, a Roth IRA provides tax-free withdrawals. The key is consistency; redirecting even a small portion of your childfree savings surplus into these accounts builds substantial long-term wealth.

Leverage the HSA triple tax advantage

The Health Savings Account (HSA) is often overlooked but offers the best tax treatment of any retirement vehicle. Contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. If you can afford to pay current medical bills out-of-pocket, let your HSA grow. It effectively becomes a supplemental retirement account that protects you against rising healthcare costs in later life.

Tools to streamline your savings

Automating these contributions removes the temptation to spend the extra income. Use financial planning tools to track your progress against your specific childfree retirement goals. Below are recommended resources to help you set up and manage these accounts effectively.

As an Amazon Associate, we may earn from qualifying purchases.

Design your estate plan

Without children as default heirs, your estate plan requires intentional structure to ensure your assets are distributed according to your wishes. This involves appointing trusted agents for financial and medical decisions, rather than relying on automatic legal defaults.

Key Estate Planning Components

- Will or Trust: Establish a legal document outlining asset distribution. A revocable living trust can help avoid probate, keeping your affairs private and potentially faster to settle.

- Durable Power of Attorney: Designate someone to manage your finances if you become incapacitated. Without children, this person is often a sibling, close friend, or professional fiduciary.

- Healthcare Proxy: Appoint an agent to make medical decisions on your behalf. Ensure this person understands your values regarding end-of-life care.

- Beneficiary Designations: Review all retirement accounts, life insurance policies, and bank accounts. These assets bypass your will, so ensure beneficiaries are current and appropriate.

-

Draft or update your will or trustEnsure your asset distribution reflects your current wishes and relationships.

-

Appoint a financial power of attorneyChoose a trusted individual to manage finances if you are unable to do so.

-

Designate a healthcare proxySelect someone to make medical decisions aligned with your values.

-

Review beneficiary designationsUpdate all retirement accounts, insurance policies, and bank accounts.

Plan for long-term care

Childfree individuals often face unique challenges in long-term care planning, as they may lack family members to provide informal care or manage affairs. Proactive planning is essential to ensure financial security and quality of life in later years.

Strategies for Long-Term Care

- Long-Term Care Insurance: Consider policies that cover nursing home care, assisted living, or in-home care. This can protect your assets from being depleted by high care costs.

- Hybrid Life Insurance Policies: These combine life insurance with long-term care benefits, offering a death benefit if care is not needed, or care benefits if it is.

- Self-Funding: If you have substantial assets, you might choose to self-fund care. This requires careful investment planning to ensure your portfolio can sustain high expenses over a potentially long period.

- Community and Social Networks: Build strong social connections. Friends and community groups can provide emotional support and practical assistance, reducing reliance on formal care systems.

Fund your lifestyle goals

Financial planning without children 2026 isn't just about hoarding capital; it's about converting surplus funds into tangible life quality. When you remove the heavy burden of college tuition and child-rearing costs, you gain the freedom to allocate resources toward luxury travel, high-end experiences, and deep hobbies. This section shows you how to structure that spending so it enhances your daily life rather than draining your long-term security.

Treat lifestyle spending as a fixed line item, not a leftover. Calculate a monthly or annual amount for travel and hobbies that feels significant but sustainable. For example, if you have $1,000 in monthly surplus, allocate $300 specifically for "life enrichment"—be it a weekend ski trip, a cooking class, or a gallery membership. This prevents lifestyle creep from eroding your investment portfolio.

Prioritize spending that compounds in joy. Instead of one-off purchases, fund memberships, subscriptions, or classes that you use regularly. A monthly theater subscription or a weekly golf league provides consistent value and social connection. This approach turns financial freedom into a daily habit rather than a rare event, ensuring your money actively supports your happiness throughout the year.

Treat your lifestyle budget like an investment portfolio. Review your spending every six months to see what brought you the most joy and what felt like a waste. Adjust the allocation accordingly. If you find that solo travel brings more satisfaction than group trips, shift the funds there. This dynamic adjustment ensures your money always aligns with your current values and desires.

Common questions about childfree finance

Financial planning without children requires specific adjustments to how you manage wealth, estate distribution, and long-term security. The absence of default heirs shifts the responsibility entirely onto you to appoint trusted agents and structure your assets intentionally.

No comments yet. Be the first to share your thoughts!