The Childfree Advantage: A Financial Snapshot

Many assume the greatest rewards of a childfree life are experiential – the freedom to travel, pursue hobbies, or dedicate oneself to a career. While undeniably valuable, these benefits often overshadow a powerful, often underestimated advantage: financial freedom. It’s not about lacking love or fulfillment; it’s about recognizing the significant financial commitment inherent in raising children and understanding the opportunities that open up when that commitment isn’t present.

At the heart of this advantage lies the concept of opportunity cost. Every dollar spent on one thing is a dollar not spent on another. Raising a child, while incredibly rewarding, represents a substantial financial outlay over nearly two decades. This isn’t a judgment on parenthood, but a realistic assessment of resources. For couples intentionally choosing a childfree life, those resources can be redirected towards other goals, potentially accelerating their path to financial independence.

I want to be clear: this isn't about assigning a monetary value to a child or suggesting one lifestyle is superior to another. It’s about empowering those who have chosen a childfree path to understand the potential financial implications of that decision. Recognizing this advantage allows for proactive planning and maximizing the opportunities available.

Calculating the True Cost of Kids

Let's get specific. The USDA’s report, "Cost of Raising a Child," estimated the cost of raising a child born in 2015 to age 18 at approximately $233,610, excluding post-secondary education. Adjusting for inflation to 2026, and accounting for regional variations in housing and childcare costs, that number easily climbs to over $300,000. This figure represents an average; expenses can be significantly higher in urban areas or for families prioritizing private education.

The $300,000+ estimate covers essential categories: housing (representing the largest portion, often around 30%), food, transportation, healthcare, childcare, and clothing. However, it doesn’t fully capture the hidden costs. Consider the loss of income during parental leave, the potential for reduced career advancement opportunities, and the expenses associated with extracurricular activities, summer camps, and birthday parties. These seemingly small costs add up considerably over 18 years.

College expenses are a separate, substantial burden. The average cost of tuition, fees, room, and board at a four-year public university is currently around $28,653 per year, according to EducationData.org. For a private university, that figure jumps to $57,570. Saving for college for one child could easily add another $150,000 - $250,000 to the overall cost. It’s a significant financial undertaking, and one childfree couples simply don't have to consider.

The Financial Freedom Calculator: Your Numbers

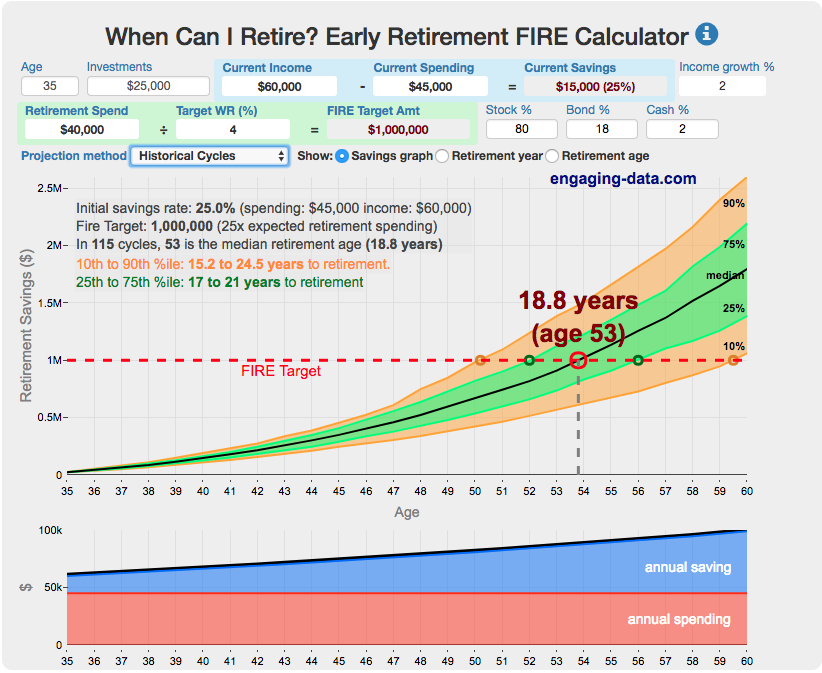

Now, let’s translate these costs into tangible projections for your situation. The power of avoiding a $300,000+ expense, combined with consistent saving and investing, is substantial. To illustrate this, consider a couple in their early 30s, earning a combined income of $150,000 per year, with $50,000 already saved. Let’s assume a moderate investment return of 7% per year.

If this couple had a child, a significant portion of their discretionary income would be diverted to childcare and other child-related expenses. However, remaining childfree allows them to continue maximizing their investments. Using a conservative estimate, they could potentially retire 10-15 years earlier, with a significantly larger nest egg. The exact number depends on their savings rate and investment choices.

A financial freedom calculator allows you to input your specific details – age, income, current savings, desired retirement age, expected investment returns – and see the projected outcome. Several free calculators are available online, such as the one offered by NewRetirement.com. Experiment with different scenarios to understand how your choices impact your financial future. The results can be genuinely shocking – for example, a consistent $1,500/month investment, instead of being allocated to childcare, could lead to a multi-million dollar portfolio.

Investing the Difference: Where Does the Money Go?

Simply saving money isn't enough; it needs to be invested wisely. Childfree couples have the advantage of a longer time horizon and potentially greater risk tolerance. A diversified portfolio consisting of stocks, bonds, and real estate is a solid foundation. Index funds and ETFs (Exchange Traded Funds) offer low-cost, diversified exposure to the market.

Don't overlook the power of tax-advantaged accounts. Maximize contributions to 401(k)s and IRAs. Consider a Health Savings Account (HSA) if eligible, as it offers triple tax benefits – contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free. The White Coat Investor provides excellent resources on optimizing these accounts for financial independence.

The key is to start early and be consistent. Compounding is your greatest ally. Even small, regular investments can grow substantially over time. Reinvest dividends and avoid the temptation to time the market. Focus on long-term growth and stay disciplined.

Beyond Retirement: Lifestyle Inflation and Big Dreams

Financial freedom isn't solely about early retirement; it's about creating a life filled with experiences and passions. Childfree couples have the resources to pursue travel, hobbies, education, and other interests without financial constraints. Imagine taking a sabbatical to learn a new skill, volunteering for a cause you care about, or traveling the world.

However, it's crucial to guard against lifestyle inflation – the tendency to increase spending as income rises. While enjoying the fruits of your labor is important, avoid letting your expenses creep up to match your income. Consciously choose where to allocate your resources and prioritize experiences over material possessions.

Many childfree couples also choose to dedicate a portion of their wealth to philanthropic endeavors. Supporting charities and causes you believe in can provide a sense of purpose and fulfillment. AARP’s resources highlight that many retirees find immense satisfaction in giving back to their communities.

Essential Reads for Childfree Financial Independence

Provides a straightforward investment strategy focused on low-cost index funds. · Explains the principles of financial independence and how to achieve it. · Offers guidance on building wealth and living a fulfilling life.

This book offers a clear and actionable investment plan designed to build wealth efficiently, making it an essential read for those pursuing financial independence.

Guides readers through nine practical steps to achieve financial independence. · Encourages a mindful approach to spending and earning. · Focuses on aligning financial goals with personal values.

This foundational text redefines your relationship with money, offering a transformative framework for achieving financial independence through conscious living.

Presents a comprehensive philosophy for achieving extreme financial independence. · Offers practical strategies for reducing expenses and increasing savings. · Explores the lifestyle implications of early retirement.

This guide provides a radical yet practical approach to financial independence, detailing how to drastically reduce expenses and accelerate wealth accumulation.

Delivers actionable advice on saving money across various aspects of life. · Provides strategies for effective debt management and financial planning. · Focuses on achieving financial well-being without sacrificing quality of life.

This guide offers essential, budget-friendly strategies for maximizing savings, eliminating debt, and enhancing your overall financial health.

Features detailed itineraries and maps for extensive European travel. · Includes insider tips from local experts. · Covers a wide range of popular European destinations.

This comprehensive travel guide empowers you to plan unforgettable journeys across Europe, leveraging expert insights and detailed resources to maximize your travel experiences.

As an Amazon Associate I earn from qualifying purchases. Prices may vary.

Common Pitfalls & Staying on Track

Even with careful planning, financial setbacks can occur. Common mistakes childfree couples make include underestimating future expenses (healthcare costs in retirement are often higher than anticipated), taking on too much debt, and failing to diversify their investments. Market downturns can be particularly challenging, but it's important to remain calm and avoid making rash decisions.

Regular financial check-ups are essential. Review your budget, investment portfolio, and financial goals at least once a year. Adjust your plan as needed to reflect changes in your circumstances or market conditions. Consider working with a financial advisor to get personalized guidance.

Don’t fall into the trap of comparing yourself to others. Everyone’s financial situation is unique. Focus on your own goals and celebrate your progress along the way. Staying disciplined and proactive is key to achieving long-term financial freedom.

Community Insights: Real Stories & Perspectives

The childfree community is full of inspiring stories of financial independence and intentional living. Many couples share their experiences online, offering valuable insights and support. One couple, Sarah and David, shared that choosing a childfree life allowed them to pay off their mortgage 15 years early and pursue their passion for travel.

Another member of our community, Emily, used her savings to start her own business. She emphasized the importance of having a financial cushion to take risks and pursue her entrepreneurial dreams. These stories demonstrate the diverse ways childfree couples can leverage their financial freedom to create fulfilling lives.

Connecting with others who share your values can provide motivation and accountability. Join online forums, attend workshops, or participate in local events to learn from and support fellow childfree individuals.

No comments yet. Be the first to share your thoughts!