Childfree & FIRE: The Rising Trend

More people are choosing a life without children, and this decision impacts their financial trajectories. It's a reshaping of priorities and an acceleration toward financial independence. The FIRE (Financial Independence, Retire Early) movement is gaining momentum, and childfree individuals are well-positioned to achieve its goals.

Freedom from the costs of raising a family allows for redirecting resources toward investments and accelerated savings. This acknowledges the financial realities of different life choices. The CalPERS PERSpective reported in 2021 that individuals without children show different savings patterns compared to those with children, a trend likely to continue.

The rise in intentional childfree living links to changing societal norms, increased educational and career opportunities for women, and growing awareness of global challenges. This demographic often shows self-determination and a desire to design a life aligned with their values, including financial security and early retirement. A life intentionally lived, on one's own terms, is a strong driver.

Understanding this trend means recognizing that FIRE isn’t just about deprivation; it’s about intentionality. It’s about optimizing resources to achieve freedom that allows for pursuing passions, contributing to society, or enjoying life without the constraints of traditional employment. This is increasingly appealing, especially among younger generations.

The Childfree Financial Advantage

The financial benefits of remaining childfree are substantial and often underestimated. Raising a child is expensive. The USDA estimated in 2015 that the cost of raising a child to age 18 is approximately $233,610, excluding college expenses. Current estimates, factoring in inflation, exceed $300,000. This figure doesn’t include ongoing costs for higher education, extracurricular activities, or healthcare.

Consider the breakdown: housing costs increase with a growing family, requiring larger homes or moves to different school districts. Food expenses rise with each additional mouth to feed. Healthcare costs, even with insurance, can be substantial, especially during childhood illnesses. Education, both private and public, is a significant financial burden. These expenses accumulate over decades.

The AARP notes that individuals without children often have a greater capacity for long-term savings and investment. By redirecting funds that would have gone to child-related expenses, childfree individuals can accelerate their progress toward financial independence. This could involve increasing contributions to retirement accounts, investing in real estate, or pursuing other wealth-building strategies.

This isn’t about devaluing parenthood. It’s about acknowledging the financial implications of different life choices. Recognizing this advantage allows childfree individuals to make informed decisions and maximize their potential for early retirement. It’s a matter of opportunity cost – what could those resources achieve if directed elsewhere?

Aggressive Savings & Investment Strategies

Maximizing your savings rate is paramount when pursuing FIRE. Aim for a savings rate of 50-70% of your income – a challenging but achievable goal for many childfree individuals. This requires diligent budgeting, mindful spending, and a commitment to prioritizing financial goals. The higher your savings rate, the faster you'll accumulate wealth and reach financial independence.

Investment vehicles are crucial. Diversification is key; don’t put all your eggs in one basket. Consider a mix of stocks, bonds, real estate, index funds, and Exchange Traded Funds (ETFs). Index funds, like those offered by Vanguard and Fidelity, provide broad market exposure at low cost. ETFs offer similar benefits with greater flexibility. Real estate can provide both income and appreciation, but requires careful consideration of property management and market conditions.

The power of compound interest cannot be overstated. Starting early is a significant advantage. Even small, consistent investments can grow substantially over time. A $500 monthly investment earning an average annual return of 7% can grow to over $500,000 in 30 years. Utilize tax-advantaged accounts to maximize your returns. Contribute the maximum amount to your 401(k) and IRA each year.

Health Savings Accounts (HSAs) offer a triple tax advantage – contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. This makes them an excellent vehicle for long-term healthcare savings. Avoid chasing get-rich-quick schemes or speculative investments. A long-term, diversified approach is the most reliable path to financial independence. Consistency is more important than trying to time the market.

Optimizing Your Lifestyle for FIRE

FIRE isn’t solely about maximizing income and minimizing expenses; it’s about designing a lifestyle that aligns with your values and supports your financial goals. Reducing expenses doesn’t necessarily mean sacrificing quality of life; it means making conscious choices about where your money goes. Consider strategies like house hacking – renting out a portion of your home to generate income – or minimalist living, which prioritizes experiences over material possessions.

Travel hacking, using credit card rewards and travel deals to reduce travel costs, can be a significant expense saver. Prioritize experiences that bring you joy and fulfillment, rather than accumulating unnecessary possessions. Embrace frugal habits, such as cooking at home, using public transportation, and finding free or low-cost entertainment options.

Increasing your income streams is equally important. Explore side hustles that align with your skills and interests. This could include freelance work, online tutoring, or starting a small business. The additional income can be used to accelerate your savings and investments. The more income you generate, the faster you'll reach financial independence.

"Early retirement’ doesn"t always mean complete cessation of work. Many FIRE adherents transition to part-time work, consulting, or pursuing passion projects that generate income. The goal is to gain financial freedom and the ability to choose how you spend your time, not necessarily to stop working altogether. This is about freedom and flexibility, not necessarily complete withdrawal from the workforce.

- House hacking

- Minimalist living

- Travel hacking

- Side hustles

Navigating Healthcare Costs

Healthcare is a significant concern for early retirees, particularly those under the age of 65 and ineligible for Medicare. Bridging the gap between retirement and Medicare eligibility requires careful planning and financial preparation. The Affordable Care Act (ACA) marketplace offers health insurance options, but premiums can be substantial. Exploring different plans and using subsidies can help reduce costs.

Health Savings Accounts (HSAs) are a valuable tool for managing healthcare expenses. Contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. This makes them an excellent way to save for future healthcare costs. Consider a high-deductible health plan (HDHP) to qualify for HSA contributions.

Private insurance is another option, but premiums can be significantly higher than ACA plans. Long-term care insurance should also be considered, as the cost of long-term care can be substantial. Be realistic about potential healthcare expenses and factor them into your financial plan. It’s better to overestimate than underestimate.

It’s crucial to research and compare different healthcare options to find the best coverage at the most affordable price. Don’t neglect preventative care, as it can help avoid costly medical expenses down the road. Healthcare costs are a major variable in early retirement planning, so thorough preparation is essential.

Location, Location, Location

Where you choose to live significantly impacts your cost of living and your ability to achieve FIRE. The cost of housing, transportation, food, and healthcare varies dramatically between cities and states. Moving to a lower-cost area can dramatically accelerate your progress toward financial independence. Consider factors like taxes, healthcare access, and lifestyle preferences when evaluating potential locations.

States with no state income tax, such as Florida, Texas, and Nevada, can offer significant tax savings. However, property taxes may be higher in these states. Research the overall cost of living in different areas to determine which locations best suit your needs and budget. Websites like Numbeo and BestPlaces provide cost of living comparisons.

Some cities and states are particularly FIRE-friendly due to their low cost of living and access to outdoor activities. Examples include Boise, Idaho; San Antonio, Texas; and Asheville, North Carolina. International locations, such as Portugal, Mexico, and Panama, can also offer a lower cost of living and a desirable lifestyle.

Consider your lifestyle preferences when choosing a location. Do you prefer a bustling city or a quiet rural setting? Do you enjoy outdoor activities or cultural events? Choose a location that aligns with your values and interests to maximize your quality of life. This is about more than just numbers; it's about creating a fulfilling life.

Qualitative Comparison of FIRE-Friendly Locations (2026)

| City/State | Cost of Living | Taxes | Healthcare Access | Lifestyle/Amenities |

|---|---|---|---|---|

| Austin, TX | High | Medium | High | High |

| Boise, ID | Medium | Medium | Medium | Medium |

| Portugal | Medium | Medium | High | High |

| Mexico City | Low | Medium | Medium | High |

| Asheville, NC | Medium | Medium | Medium | High |

| Valencia, Spain | Medium | Medium | High | High |

| Chiang Mai, Thailand | Low | Low | Medium | High |

Illustrative comparison based on the article research brief. Verify current pricing, limits, and product details in the official docs before relying on it.

Staying the Course: Maintaining FIRE

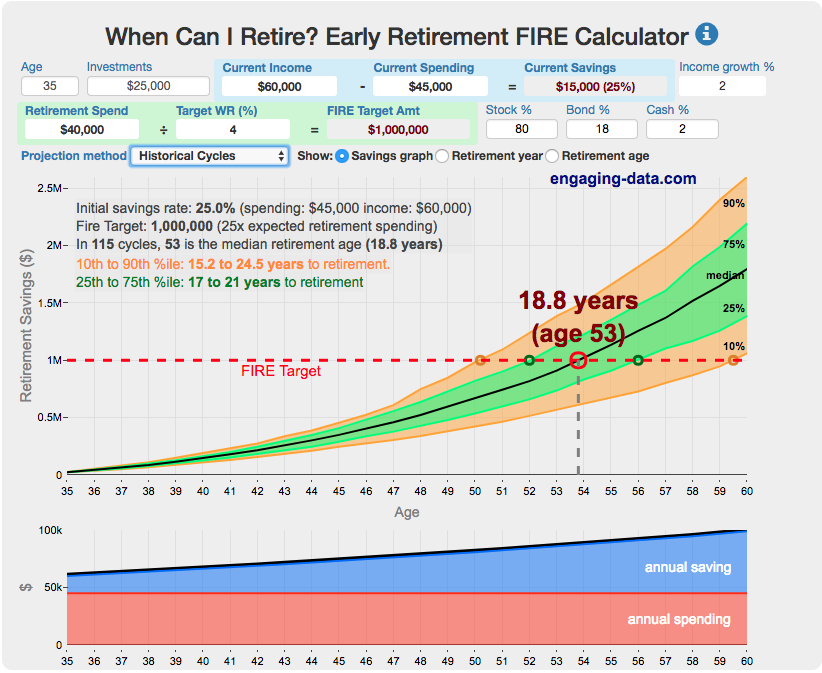

Achieving FIRE is only the first step. Maintaining financial independence throughout retirement requires ongoing financial monitoring and adjustments. The 4% rule – withdrawing 4% of your portfolio each year – is a commonly used guideline, but it's not foolproof. Market downturns, inflation, and unexpected expenses can all impact your portfolio's sustainability.

It’s crucial to regularly review your withdrawal rate and adjust it as needed. Consider a more conservative withdrawal rate, such as 3% or 3.5%, to increase the longevity of your portfolio. Diversification remains key, even in retirement. Continue to invest in a mix of stocks, bonds, and other assets to mitigate risk.

Inflation is a significant threat to financial independence. Plan for rising prices by including inflation-protected securities in your portfolio. Be prepared to adjust your spending habits if inflation erodes your purchasing power. Unexpected expenses are inevitable. Maintain an emergency fund to cover unforeseen costs.

The psychological aspects of early retirement are often underestimated. Finding purpose and fulfillment in retirement is essential for long-term happiness. Explore new hobbies, volunteer your time, or pursue passion projects. Maintaining social connections and staying active are also important. FIRE is about freedom, but it also requires intentionality and a commitment to living a meaningful life.

Childfree FIRE Standouts: Real-Life Examples

Let's look at some inspiring examples. Sarah, a former software engineer, achieved FIRE at age 42 by aggressively saving 70% of her income and investing in low-cost index funds. She now dedicates her time to volunteering at an animal shelter and traveling the world. Her story demonstrates the power of disciplined saving and a minimalist lifestyle.

Mark and Lisa, a couple who both work in the healthcare industry, retired at age 45 by focusing on real estate investing and side hustles. They purchased several rental properties, which generate passive income, and started a successful online business. Their story highlights the benefits of diversifying income streams and leveraging entrepreneurial opportunities.

David, a former teacher, retired at age 43 by embracing a frugal lifestyle and maximizing his contributions to tax-advantaged accounts. He now spends his time writing, gardening, and pursuing his passion for photography. His story demonstrates that FIRE is achievable even on a modest income with careful planning and dedication. These individuals are proof that a childfree life can unlock significant financial freedom.

No comments yet. Be the first to share your thoughts!