The Childfree Wealth Gap: 2026 Data

Financial analysis from 2024-2026 shows childfree millennials accumulating wealth faster than parents, especially in investments and home equity. A comparative analysis of millennial net worth confirms a significant difference based on parental status.

A National Bureau of Economic Research study in late 2025 found childfree millennials have 28% more net worth than parents, even when controlling for income and education. This gap stems from the significant financial resources saved by not raising a family. Individual circumstances vary, but the trend is clear.

This wealth gap affects housing markets, investment strategies, and retirement timelines. Childfree millennials are positioned to achieve financial independence earlier, changing traditional ideas about wealth accumulation and life stages. This acknowledges a clear economic outcome, not a judgment of lifestyle choices.

Expense Differences: Where the Money Goes

Raising children has a substantial financial impact beyond obvious expenses. Diapers and formula are significant, but only part of the picture. The USDA estimates raising a child to age 18 in 2026 costs about $328,000, not including college. This figure also misses less tangible costs, like lost income when a parent reduces work hours.

Ripple effects include larger housing needs, increased healthcare costs (even with insurance), and extracurricular activities. Parents also face the 'opportunity cost' of delaying career advancement or leaving the workforce. A two-income household can dedicate a significant portion of earnings to childcare, potentially over $20,000 annually depending on location and child's age.

Childfree millennials' discretionary spending often prioritizes experiences like travel, hobbies, and personal development, alongside investments. These expenses are typically far lower than ongoing child-rearing costs. Many childfree individuals allocate a larger income percentage to retirement accounts and long-term investments.

- Childcare: $10,000 - $20,000+ per year

- Healthcare: Increased premiums and out-of-pocket expenses

- Housing: Larger homes or more expensive neighborhoods

- Education: Private school, tutoring, college savings

- Activities: Sports, music lessons, camps

Average Annual Expenses - Parents vs. Childfree Millennials (Ages 25-35) - 2026 Estimates

| Expense Category | Parents (Average) | Childfree Millennials (Average) |

|---|---|---|

| Housing | $28,500 | $22,000 |

| Transportation | $11,000 | $8,500 |

| Food | $14,000 | $7,000 |

| Healthcare | $6,500 | $6,000 |

| Childcare/Education | $18,000 | $0 |

| Entertainment | $4,500 | $6,000 |

| Savings/Investments | $5,000 | $15,000 |

Illustrative comparison based on the article research brief. Verify current pricing, limits, and product details in the official docs before relying on it.

Investment Strategies: Time & Flexibility

Financial freedom from being childfree allows for more aggressive, longer-term investment strategies. Without the immediate financial obligations of raising children, individuals can take more risk and capitalize on compounding interest. Early, consistent investing is a cornerstone of wealth building.

Childfree millennials often favor index funds and ETFs for diversified stock market exposure with low fees. Real estate is also popular, without the pressure of finding family-friendly neighborhoods or larger properties. The White Coat Investor recommends maximizing tax-advantaged accounts (401(k)s, IRAs, HSAs) for accelerated wealth accumulation.

This is about time as much as money. Staying invested long-term, without needing funds for unexpected childcare or education costs, is a significant advantage. Consistent, disciplined investing over decades yields substantial returns, enabling early retirement or financial independence.

Homeownership & Location Choices

Childfree millennials have greater flexibility in choosing where to live, significantly impacting housing costs. Unlike parents prioritizing school districts, childfree individuals can prioritize lifestyle, career opportunities, or amenities. This freedom allows them to avoid expensive areas with highly-rated schools, potentially saving hundreds of thousands of dollars.

A growing trend sees childfree individuals choosing urban centers, prioritizing walkability, cultural attractions, and career access over large yards and suburban sprawl. This often means smaller, more affordable housing like condos or townhouses. Some downsize or opt for less expensive housing in desirable locations, further reducing expenses.

Property values are also impacted. Family-friendly neighborhoods often command a premium, while areas popular with childfree individuals may see different appreciation patterns. This flexibility in location and housing choice drives wealth accumulation for this demographic.

Career Advancement & Earning Potential

Being childfree can positively impact career trajectories. The ability to work longer hours, relocate for opportunities, and pursue further education or training without childcare constraints can lead to faster career advancement and increased earning potential. Parents can achieve career success, but the absence of these constraints offers an advantage.

Childfree status correlates with higher educational attainment, particularly for women. A 2024 Pew Research Center study found childfree women are more likely to have graduate degrees than mothers. This increased education often translates to higher earning potential.

This isn't a universal experience and doesn't perpetuate gender stereotypes. However, prioritizing career development without the demands of parenthood can contribute to increased earning potential and wealth accumulation.

Content is being updated. Check back soon.

Estate Planning: Beyond Inheritance

Estate planning is crucial for everyone, but it differs for childfree individuals and couples. Without direct descendants, the focus shifts from inheritance to charitable giving or leaving assets to family, friends, or organizations. A comprehensive estate plan ensures assets are distributed per your wishes and minimizes tax liabilities.

Wills, trusts, and beneficiary designations are essential estate planning components. A will outlines asset distribution upon death, while a trust offers more control over timing and manner. Regularly reviewing and updating beneficiary designations on retirement accounts and insurance policies is critical.

Davis Schilken, PC suggests considering estate tax implications and exploring strategies to minimize them. Options include charitable remainder trusts or gifting assets during your lifetime. Careful planning ensures your legacy reflects your values and supports your chosen causes.

- Create a Will: Designate beneficiaries and executors.

- Establish a Trust: For greater control and potential tax benefits.

- Review Beneficiary Designations: Ensure they align with your wishes.

- Consider Charitable Giving: Support causes you care about.

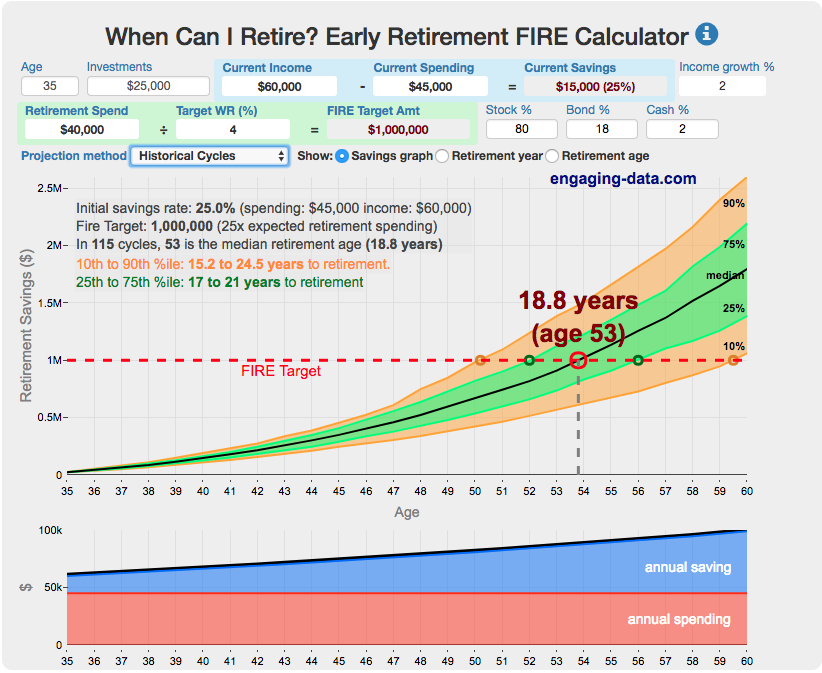

Early Retirement & Financial Freedom

Increased savings, investment gains, and lower expenses allow childfree millennials to pursue early retirement or financial independence more readily. The FIRE (Financial Independence, Retire Early) movement offers a roadmap for achieving financial freedom through disciplined saving and investing.

Realistic retirement timelines vary depending on individual circumstances and financial goals, but it’s not uncommon for childfree millennials to aim for retirement in their 50s or even earlier. This requires a high savings rate, strategic investment choices, and a commitment to living below your means. A common rule of thumb is the '4% rule,' which suggests withdrawing 4% of your retirement savings each year.

For example, a couple with $1.5 million in retirement savings could theoretically withdraw $60,000 per year without depleting their principal. The specific amount needed for retirement depends on lifestyle, healthcare costs, and other factors, but the financial foundation laid by a childfree lifestyle significantly increases the probability of achieving early retirement.

Navigating Societal Expectations

Childfree individuals often face societal pressures and financial advice geared towards parents. Navigating these expectations requires a strong sense of self-awareness and a commitment to staying focused on personal financial goals. It’s important to remember that there’s no one-size-fits-all approach to life or finance.

Building a supportive community of like-minded individuals can provide encouragement and validation. Connecting with others who share similar values and priorities can help you navigate societal expectations and stay motivated on your financial journey. Remember that your choices are valid, and your financial well-being is paramount.

What's the biggest financial benefit of being childfree, in your experience?

Vote below. If you select Other, share your answer in the text field.

No comments yet. Be the first to share your thoughts!