The Childfree Advantage: Retirement Starts Earlier

There’s a quiet revolution happening, and it’s fueled by financial freedom. More and more people are questioning traditional life paths, and for many, that includes opting out of parenthood. This isn’t about making a judgment on anyone's choices – it's about recognizing the significant financial impact that having children can have, and how choosing a childfree life can unlock opportunities for early retirement. We’re talking about aiming for 45, or even earlier, a goal that feels increasingly attainable when you’re not factoring in the costs of raising a family.

The idea of retiring at 45 might sound radical, but it’s becoming a reality for a growing number of people, particularly those embracing the FIRE – Financial Independence, Retire Early – movement. It’s a shift in mindset, prioritizing experiences and financial security over societal expectations. It’s about redefining success on your own terms. For those who choose not to have children, the financial flexibility this affords is a huge advantage, allowing for faster progress towards these goals.

Choosing a childfree life is a deeply personal decision, and it shouldn’t be framed as a prerequisite for financial success. However, it is a significant financial decision with long-term implications. The money that would have been spent on raising children can be redirected towards investments, experiences, or simply a more comfortable retirement. This isn’t about deprivation; it’s about intentionality and maximizing your options.

We’re seeing a cultural shift, too. Younger generations are less focused on ticking off traditional boxes – marriage, house, kids – and more interested in travel, personal growth, and pursuing passions. This shift is creating a space for alternative life paths, and early retirement is becoming a more popular aspiration. It’s a rejection of the "work until you’re 65’ model and a desire for more control over one"s time and destiny.

Calculating Your 'Kids Cost': A Realistic Look

Let’s get real about the numbers. The cost of raising a child is substantial, and often underestimated. According to the USDA, in 2015, it cost roughly $233,610 to raise a child to age 18, not including college. Adjusting for inflation, that number is closer to $300,000 in 2024. AARP highlights that these figures don’t include the lost income from a parent taking time off work, which can add significantly to the overall cost.

These expenses break down into several key categories. Housing is a major factor – you might need a larger home, or move to a more expensive school district. Food costs increase with each growing child. Healthcare expenses, including doctor visits, vaccinations, and potential emergencies, add up quickly. Childcare is often the biggest single expense, especially for younger children, potentially costing upwards of $20,000 per year in many areas.

Education is another significant cost. Beyond the cost of K-12 schooling, you have to consider potential college expenses. The average cost of tuition, fees, room, and board at a private university is around $60,000 per year (according to EducationData.org, 2024), and even public universities are becoming increasingly expensive. Activities, from sports to music lessons to summer camps, also contribute to the overall cost. These aren’t luxuries; they're often seen as essential for a child’s development.

Now, it’s true that you can reduce these costs through careful budgeting, thriftiness, and choosing affordable options. But realistically, even with those efforts, raising a child is a significant financial undertaking. The savings potential for a childfree couple can range from a conservative $200,000 to an aggressive $500,000 or more over the course of a lifetime. That’s money that can be invested and compounded, accelerating your path to early retirement.

Aggressive Saving & Investing: The FIRE Framework

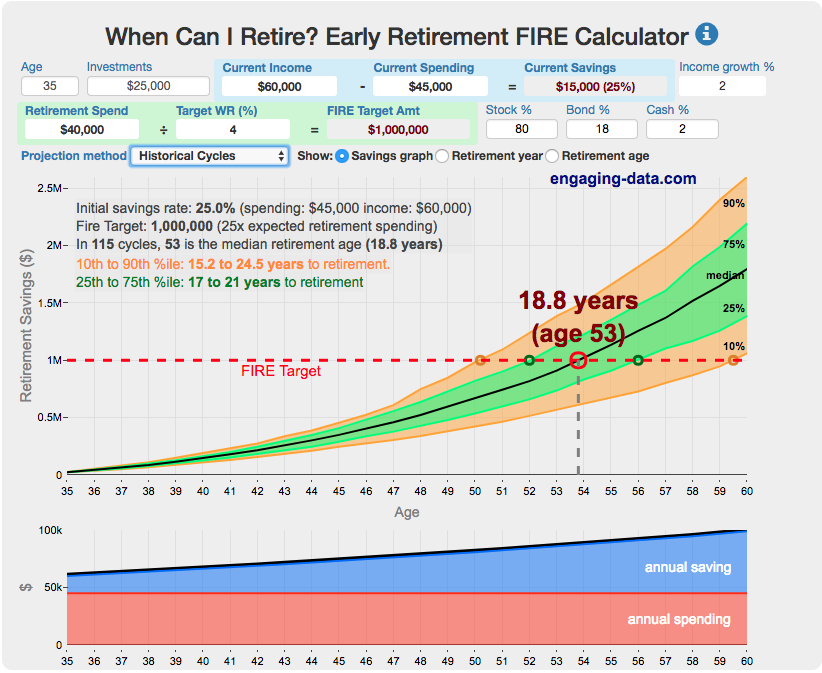

The FIRE (Financial Independence, Retire Early) movement provides a roadmap for achieving early retirement. At its core, FIRE is about maximizing your savings rate – the percentage of your income that you save and invest – and living below your means. The higher your savings rate, the faster you’ll reach financial independence. For those with the added financial boost of being childfree, hitting a 50% or even 70% savings rate is often achievable.

There are different paths within the FIRE movement. Lean FIRE involves extreme frugality and a modest retirement lifestyle. Fat FIRE aims for a luxurious retirement, requiring a larger nest egg. Barista FIRE involves partially retiring and working a part-time job to cover expenses while living off your investments. The best path for you will depend on your lifestyle preferences and financial goals.

Maximizing investment contributions is crucial. Take full advantage of tax-advantaged accounts like 401(k)s and IRAs (both traditional and Roth). Contribute enough to your 401(k) to get the full employer match – it’s free money! Consider maxing out your IRA contributions each year. In 2024, the IRA contribution limit is $7,000, or $8,000 if you're age 50 or older.

Asset allocation is also key. Diversify your investments across different asset classes – stocks, bonds, real estate – to reduce risk. Your risk tolerance should influence your investment choices. Younger investors with a longer time horizon can generally afford to take on more risk, while those closer to retirement may prefer a more conservative approach. Consider using low-cost index funds and ETFs to build a diversified portfolio.

Real Estate: A Powerful Childfree Accelerator

Real estate can be a powerful tool for accelerating your early retirement journey. Homeownership offers the opportunity to build equity over time, and potentially generate rental income. However, it’s not a one-size-fits-all solution. Carefully consider the pros and cons of buying versus renting.

One strategy to consider is house hacking. This involves renting out rooms in your primary residence, or purchasing a multi-family property and living in one unit while renting out the others. This can significantly reduce your housing expenses and generate passive income. Another option is to invest in rental properties, but this requires more active management and comes with its own set of risks.

The risks associated with real estate include property taxes, maintenance costs, potential vacancies, and the possibility of property values declining. Location is also crucial. Invest in areas with strong rental demand and potential for appreciation. Research local market trends and consider factors like school districts, crime rates, and job growth.

Real estate isn’t for everyone. It requires capital, time, and effort. If you’re not comfortable with the responsibilities of property ownership, renting might be a better option. However, for those willing to put in the work, real estate can be a valuable asset in your early retirement plan.

Homeownership vs. Renting: A Childfree Early Retirement Perspective

| Factor | Homeownership | Renting |

|---|---|---|

| Financial Benefits 💰 | Potentially High (equity building, tax deductions – consult a tax professional) | Medium (predictable monthly costs, no major repair bills) |

| Flexibility ✈️ | Low (less mobile, selling can be time-consuming and costly) | High (easier to relocate for travel or opportunities) |

| Responsibility 🛠️ | High (maintenance, repairs, property taxes, insurance) | Low (landlord responsible for most maintenance) |

| Long-Term Security 🏡 | Medium to High (stable housing, potential asset growth – market dependent) | Medium (security relies on landlord and lease terms) |

| Upfront Costs 💸 | High (down payment, closing costs, moving expenses) | Low to Medium (security deposit, first month’s rent) |

| Impact on Savings 📈 | Can be positive with equity, but significant expenses can hinder savings | Generally allows for higher savings rate due to lower fixed costs |

| Retirement Income Potential 💰 | Potential to downsize and utilize home equity in retirement | Requires separate investment strategies for retirement housing |

Illustrative comparison based on the article research brief. Verify current pricing, limits, and product details in the official docs before relying on it.

Side Hustles & Income Diversification

Relying on a single income stream is risky, especially when pursuing early retirement. Supplementing your income with side hustles can provide a financial cushion and accelerate your progress. The key is to choose a side hustle that aligns with your interests and skills.

There are countless side hustle opportunities available. Freelancing – offering your skills as a writer, designer, developer, or consultant – is a popular option. Online courses and blogging can generate passive income. E-commerce – selling products online – allows you to tap into a global market. Other ideas include virtual assistant work, social media management, and tutoring.

Remember to account for taxes on your side hustle income. You’ll likely need to pay self-employment taxes, so factor that into your earnings. Keep accurate records of your income and expenses, and consult with a tax professional if needed. Diversifying your income streams not only provides financial security but also expands your skillset and opens up new opportunities.

The beauty of side hustles is the flexibility they offer. You can work on your own schedule and choose projects that fit your lifestyle. This is particularly appealing for those pursuing early retirement, as it allows you to maintain a sense of purpose and engagement without being tied to a traditional 9-to-5 job.

Healthcare Costs: The Biggest Unknown

Healthcare costs are often the biggest unknown in early retirement planning. Accessing affordable healthcare before Medicare eligibility (age 65) can be a significant challenge. Understanding your options is crucial.

The Affordable Care Act (ACA) marketplace offers health insurance plans to individuals and families. Subsidies are available to help lower premiums, based on your income. Health Savings Accounts (HSAs) are another valuable tool, allowing you to save pre-tax dollars for healthcare expenses. COBRA – continuing your employer-sponsored health insurance – is an option, but it’s typically very expensive.

Some individuals explore international healthcare options, seeking more affordable care in countries with lower costs. However, this requires careful research and consideration of potential logistical challenges. The healthcare landscape is constantly evolving, so stay informed about policy changes and potential reforms.

Budgeting for unexpected medical expenses is essential. Even with health insurance, you may be responsible for deductibles, co-pays, and out-of-pocket costs. Building an emergency fund specifically for healthcare expenses can provide peace of mind.

Lifestyle Inflation: The Silent Retirement Killer

Lifestyle inflation is a sneaky threat to early retirement plans. It’s the tendency to increase your spending as your income increases. A new job, a promotion, or a successful side hustle can all lead to lifestyle inflation if you’re not careful.

The problem with lifestyle inflation is that it erodes your savings rate. If you’re constantly upgrading your possessions and indulging in more expensive experiences, you’ll have less money to invest. This can significantly delay your retirement goals. Combatting lifestyle inflation requires mindful spending, tracking your expenses, and setting clear financial goals.

Prioritize experiences over material possessions. Travel, learning new skills, and spending time with loved ones often bring more lasting happiness than buying the latest gadgets. Cultivate a simple and fulfilling lifestyle that aligns with your values. Remember why you’re pursuing early retirement in the first place – to gain more freedom and control over your time.

Maintaining Momentum: Staying on Track

Early retirement planning is a marathon, not a sprint. Maintaining momentum and staying motivated requires discipline and a long-term perspective. Set realistic goals and celebrate milestones along the way. Acknowledge your progress and reward yourself for achieving your targets.

Build a supportive community. Connect with other individuals who are pursuing similar goals. Share your experiences, learn from others, and provide encouragement. Online forums, social media groups, and local meetups can all be valuable resources. Remember that setbacks are inevitable. Don’t let a temporary hurdle derail your progress.

Regularly review and adjust your plan. Your financial situation and goals may change over time. Make sure your investment strategy and budget remain aligned with your objectives. Be flexible and willing to adapt to changing circumstances. Early retirement is a journey, not a destination. Enjoy the process and embrace the freedom it offers.

There are many resources available to help you on your journey. Books, podcasts, blogs, and financial advisors can provide valuable insights and guidance. Continue learning and expanding your knowledge. The more informed you are, the better equipped you’ll be to achieve your early retirement dreams.

No comments yet. Be the first to share your thoughts!