Beyond Diapers: The Childfree Financial Edge

Let’s be real: most people understand that having kids is expensive. But it’s easy to get stuck on the direct costs – the diapers, the daycare, the college fund. What often gets overlooked is the opportunity cost. That time, energy, and yes, money, could be channeled into other things. Things like early retirement, travel, or simply building a life you love without financial stress.

For those choosing a childfree life, there’s a unique opportunity to accelerate wealth building. We’re often told to plan for our children’s future, but what about prioritizing our own? According to recent analyses, the financial advantages can be significant. In fact, couples without children can potentially build wealth up to 40% faster than their counterparts with kids.

Now, it's important to be upfront: that 40% is an average. Individual results will vary depending on investment choices, market conditions, and lifestyle. But it’s a powerful illustration of the financial freedom that comes with intentionally choosing a different path. This isn’t about judgment, it’s about recognizing the power of intentionality.

Over the next few sections, we’ll break down the numbers, explore strategic investment options, and show you how to leverage your childfree status to create a financially secure and fulfilling life. We’ll look at everything from maximizing savings to planning for a retirement that truly reflects your dreams.

The Numbers Don't Lie: Quantifying the Childfree Advantage

Let's get down to brass tacks. The cost of raising a child is substantial. According to Northern Trust, the average cost of raising a child to age 18 now exceeds $300,000. That figure includes housing, food, transportation, healthcare, education, and all those extracurricular activities. And that's just the cash outlay; it doesn't factor in lost income from a parent taking time off work.

But what if that $300,000 (or more!) was invested instead? Let's consider a scenario. A couple consistently invests $15,000 per year – roughly the annual cost of childcare, according to Childfree Wealth – for 30 years, earning an average annual return of 7%. That’s a conservative estimate; historical stock market returns have been higher, but it’s prudent to be cautious.

Using a compound interest calculator, we find that this investment would grow to approximately $970,000 after 30 years. Now, compare that to a couple who spends that same $15,000 annually on raising a child. While the emotional rewards of parenthood are immeasurable, the financial outcome is significantly different. It's not about saying one choice is better than the other, it's about acknowledging the trade-offs.

It’s crucial to remember that investment returns aren't guaranteed. Market fluctuations can impact your earnings. However, consistently investing, even smaller amounts, over a long period can make a massive difference. The power of compounding is your friend here. A small change in your monthly spending can lead to huge gains over decades.

To illustrate, let's examine two scenarios: Scenario A - a couple invests $15,000 per year for 30 years. Scenario B – a couple spends $15,000 per year on raising a child and invests nothing. The difference in potential wealth accumulation is striking. The key takeaway is that financial planning without children allows for a greater capacity for long-term investment.

Strategic Allocation: Where to Put Your Extra Funds

Okay, you’ve identified the extra funds. Now what? Simply having more money isn’t enough; you need a plan for how to make it grow. The cornerstone of any sound investment strategy is diversification. Don’t put all your eggs in one basket. Spread your investments across different asset classes to mitigate risk.

Consider a mix of stocks, bonds, and real estate. Stocks offer the potential for higher returns but also come with greater volatility. Bonds are generally more stable but offer lower returns. Real estate can provide both income and appreciation potential. The ideal allocation will depend on your risk tolerance and time horizon.

Don’t overlook the importance of tax-advantaged accounts. Maximize your contributions to 401(k)s, IRAs, and Health Savings Accounts (HSAs). These accounts offer significant tax benefits that can boost your long-term returns. For example, contributing to a traditional IRA may be tax-deductible, while a Roth IRA offers tax-free withdrawals in retirement.

Alternative investments, such as cryptocurrency or private equity, can also be considered, but they come with higher risk and should only be a small portion of your portfolio. Remember, investing isn’t about getting rich quick; it’s about building wealth steadily and sustainably. This isn't about aggressive speculation; it’s about intentional, long-term growth.

Before making any investment decisions, assess your risk tolerance honestly. Are you comfortable with the possibility of losing money in the short term? Or do you prefer a more conservative approach? Your answers will help you determine the appropriate asset allocation for your portfolio.

Early Retirement: The Freedom Factor

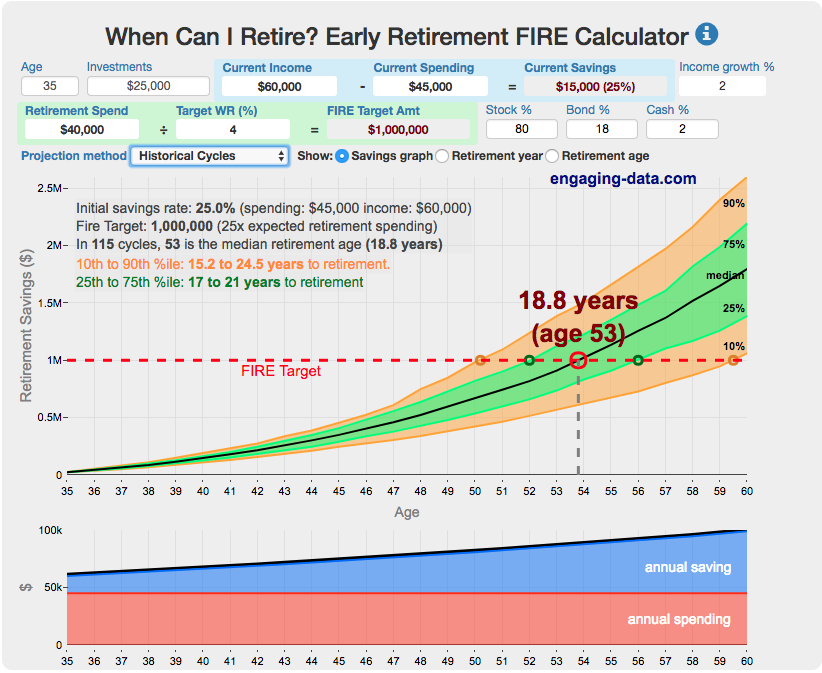

For childfree couples, the possibility of early retirement is often within reach. The FIRE (Financial Independence, Retire Early) movement has gained traction in recent years, and it aligns perfectly with the financial advantages of a childfree lifestyle. The core principle of FIRE is to save and invest a significant portion of your income, allowing you to retire decades before the traditional retirement age.

A common rule of thumb is the 4% rule: you can safely withdraw 4% of your investment portfolio each year without depleting your principal. To calculate your FIRE number, multiply your annual expenses by 25 (the inverse of 4%). For example, if you spend $60,000 per year, your FIRE number would be $1.5 million.

However, it’s crucial to factor in healthcare costs, especially if you retire early. Healthcare expenses can be significant, and you’ll need to ensure you have adequate coverage. Consider options like the Affordable Care Act (ACA) marketplace or private health insurance. Planning for healthcare is essential.

Early retirement isn’t for everyone. It requires discipline, sacrifice, and a willingness to live below your means. But for those who are committed to the lifestyle, it can offer unparalleled freedom and flexibility. It allows you to pursue your passions, travel the world, or simply enjoy life on your own terms. It’s about designing a life you love, not just working to survive.

Are You FIRE-Ready? (Childfree Edition)

So, you're rocking the childfree life and ready to *really* accelerate your path to financial independence? Awesome! 🔥 This quick quiz will help you assess your current 'FIRE readiness' – how close you are to potentially retiring early and living life on your own terms. Don't worry, it's not about perfection, it's about understanding where you stand and what steps you can take to build wealth even faster. Let's dive in!

Estate Planning: Beyond Inheritance

Estate planning is often associated with passing wealth to children, but it's equally important for childfree individuals. It’s about ensuring your wishes are honored and your assets are distributed according to your desires. Without children, you have the freedom to direct your wealth to other beneficiaries, such as charities, friends, or other family members.

Essential estate planning documents include a will, which outlines how your assets will be distributed after your death; a trust, which can provide more control over asset distribution and avoid probate; a power of attorney, which designates someone to make financial decisions on your behalf if you become incapacitated; and healthcare directives, which outline your medical wishes.

Designating beneficiaries for your accounts and insurance policies is also crucial. Regularly review and update your beneficiary designations to ensure they reflect your current wishes. Childfree Wealth emphasizes the importance of proactively planning for end-of-life care and ensuring your assets are protected.

Consider charitable giving as part of your estate plan. You can leave a lasting legacy by supporting causes you care about. There are various ways to make charitable donations, including direct gifts, bequests in your will, or charitable remainder trusts. This can offer both personal satisfaction and potential tax benefits.

Don't underestimate the importance of professional guidance. An estate planning attorney can help you navigate the complexities of estate law and ensure your plan is legally sound and tailored to your specific needs. Bragg Financial offers a range of estate planning services specifically designed for childfree adults.

Travel & Experiences: Investing in Memories

Financial planning isn’t just about accumulating wealth; it’s about living a fulfilling life. For childfree couples, this often means prioritizing travel and experiences. The freedom from financial obligations associated with raising children allows you to explore the world, pursue your passions, and create lasting memories.

Travel doesn’t have to be expensive. There are many ways to travel on a budget, such as staying in hostels, cooking your own meals, and taking advantage of free activities. Consider shoulder season travel – the periods between peak and off-peak seasons – for lower prices and fewer crowds.

Maximize your rewards points. Use travel credit cards to earn points on your everyday spending, and redeem those points for flights, hotels, or other travel expenses. Sign up for airline and hotel loyalty programs to earn additional rewards. Every little bit helps.

These experiences aren’t just enjoyable; they’re investments in your personal growth and well-being. Travel broadens your horizons, exposes you to new cultures, and creates memories that will last a lifetime. It’s about enriching your life, not just filling your bank account.

Think beyond traditional vacations. Consider taking a sabbatical, volunteering abroad, or learning a new skill. The possibilities are endless. The key is to identify what truly brings you joy and prioritize those experiences.

Content is being updated. Check back soon.

Protecting Your Future: Insurance Considerations

While you might not have dependents relying on you, insurance remains a crucial part of financial planning. Health insurance is paramount, especially in the United States where medical costs can be exorbitant. Ensure you have adequate coverage to protect yourself from unexpected medical expenses.

Life insurance may seem unnecessary without children, but it can still be valuable. It can cover debts, funeral expenses, or provide financial support to a spouse or partner. Disability insurance is equally important, protecting your income if you become unable to work due to illness or injury.

Property insurance, including homeowners or renters insurance, is essential to protect your assets from damage or loss. Consider umbrella insurance for additional liability coverage. Your insurance needs will vary depending on your individual circumstances and risk tolerance.

It's important to regularly review your insurance policies to ensure they still meet your needs. As your life changes, your insurance requirements may also change. Don't be afraid to shop around for the best rates and coverage.

The goal isn’t to live in fear of the unexpected, but to be prepared. Insurance provides a safety net, protecting your financial security and allowing you to weather life’s storms with confidence.

Staying on Track: Regular Financial Check-Ups

Financial planning isn’t a one-time event; it’s an ongoing process. Regularly monitor your progress, rebalance your portfolio, and update your financial goals. Life changes – job changes, market fluctuations, and personal circumstances – can all impact your financial plan.

Schedule regular financial check-ins – at least once a year, but ideally quarterly. Review your income, expenses, investments, and insurance coverage. Make adjustments as needed to stay on track towards your goals.

Don't hesitate to seek professional financial advice. A qualified financial advisor can provide personalized guidance and help you make informed decisions. They can also help you identify potential blind spots and optimize your financial strategy.

Remember, financial freedom is a journey, not a destination. It requires discipline, patience, and a commitment to ongoing learning. By staying proactive and informed, you can achieve your financial goals and live the life you desire.

No comments yet. Be the first to share your thoughts!